October 31 is National Caramel Apple Day in the United States

Geographic reference: United States Year: 52 weeks ended June 13, 2021 Market size: $112.13 million

What does one do with a bunch of leftover caramel candies and apples from Halloween? Make caramel apples of course! Today’s market size shows total sales for caramel/taffy apples, kits, and dips for the 52 weeks ended June 13, 2021.

In the 1950s, a Kraft Foods employee, Dan Walter, had some caramel candies left over from Halloween and a few apples. In order to use up these leftovers, he decided to melt the caramels and coat the apples with the gooey result. Voilà! The caramel apple was born! Since then, these sweet, sticky treats have become a classic autumn snack. In the 1970s, Kraft Foods introduced “Wrappies”, sheets of caramel that could be wrapped over apples, creating a quick and easy way to make caramel apples at home.

As the chart below shows, by 2021 Kraft Foods, the inventor of the caramel apple, wasn’t even in the top 5 companies by brand sales. All of these brands saw their sales increase from pre-pandemic levels, which turned out to be a boon for Marzetti and Happy Apples. Both of these brands saw sales decline from 2018 to 2019. Overall, sales increased from $88.34 million (52 weeks ended September 8, 2019) to $112.13 million (52 weeks ended June 13, 2021), a 26.9% jump.

Leading Caramel/Taffy Apple/Kit/Dip Brands, 2021

Brand (Co.)

Sales ($ mil.)

Share (%)

Growth (%)

Marzetti (T. Marzetti Co.)

44.63

39.80

+19.56

Affy Tapple (Affy Tapple LLC)

15.29

13.64

+21.64

Litehouse (Litehouse Inc.)

10.98

9.79

+97.13

Tastee (Tastee Apple Inc.)

9.02

8.04

+13.03

Happy Apples (Happy Apples Inc.)

6.71

5.98

+20.47

Other

25.50

22.74

+31.99

Sales are shown for the 52 weeks ended June 13, 2021. Sales growth is shown from the 52 weeks ended September 8, 2019. Of the brands shown, Litehouse experienced the highest growth, 97.13%. Sales grew from $5.57 million during the 52 weeks ended Septebmer 8, 2019 to $10.98 million during the 52 weeks ended June 13, 2021.

Original source: IRI Sources: Crystal Lindell, “State of the Candy Industry 2021: Novelty Sector Navigates Licensing, Changing Consumer Trends Amid COVID-19,” Candy Industry, July 30, 2021 available online here; “National Caramel Apple Day — October 31, 2021,” National Today, October 31, 2021 available online here. Image source: Henry Becerra, “candy apples, caramel, sweet on a stick, with pecans,” Unsplash, July 7, 2020 available online here.

Geographic reference: World Year: 2020 and 2028 Market size: $10.37 billion and $14.47 billion, respectively

When one thinks of cow milk alternatives, what comes to mind might be soy milk, almond milk, or the recently popular oat milk. But, this post is about a different type of alternative: goat milk. Today’s market size shows total global goat milk product revenues for 2020 and projected for 2028.

In terms of nutrition, cow milk and goat milk are nearly identical. Goat milk has more calories, protein, and fat but has fewer milligrams of cholesterol. It also has more calcium, potassium, and vitamin A. However, cow milk has more vitamin B12, selenium, and folic acid. Goat milk may be easier to digest for some people. The fat molecules are smaller, making them easier for the body to process. Also, goat milk has less lactose than cow milk. The growing popularity of this product is driven by its lower cholesterol and lactose.

In 2019, the last year for which data are available, global production of whole fresh goat milk totaled 19.9 million tons, down 2.2% from 2018, but up slightly from 2016. By region, Asia produced the most by far, 11.7 million tons, followed by Africa (4.4 million) and Europe (3.1 million). Oceania produced the least, 39 tons, followed by North America at 25,706 tons. However, North America garnered a 26.2% share of global revenues for goat milk products in 2020, the U.S. accounting for most of that. The Asia-Pacific region had a 29.8% share. There are several well-established and small goat milk producers worldwide, but the market is dominated by various international companies including Emmi Group, Kavli, Ausnutria Dairy Corp. Ltd., Granarolo Group, Dairy Goat Co-operation, Gay Lea Foods Co-operative Ltd., Hay Dairies Pte Ltd., Cherry Glen Goat Cheese Co., Goat Partners International Inc., and Summerhill Goat Dairy.

By product, milk had a 41.3% revenue share in 2020 followed by cheese and milk powder. The cheese segment is expected to grow at the highest compound annual growth rate (CAGR) through 2028. Most goat milk products are bought at supermarkets and hypermarkets. Consumers tend to feel more comfortable choosing fresh groceries, especially fresh dairy products, in person. However, online sales ranked second ahead of convenience stores. This segment benefited from the overall surge in online grocery sales during the COVID-19 pandemic and is projected to have the highest CAGR through 2028.

Sources: “Goat Milk Market Size, Share & Trends Analysis Report by Product (Milk, Milk Powder, Cheese), by Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online), by Region, and Segment Forecasts, 2021 – 2028,” Million In$ights Report Summary, April 2021 available online here; “Goat Milk Market Size Worth $14.47 Billion By 2028 | CAGR: 4.3%: Million Insights,” CISION PR Newswire, April 28, 2021 available online here; Katherine Gillen, “Goat Milk vs. Cow Milk: Is One Actually Healthier Than the Other?” PureWow Blog, August 19, 2019 available online here; “Livestock Primary,” FAOSTAT, Food and Agriculture Organization of the United Nations available online here. Image source: Rita E, “goat-pet-farm-horns-livestock-3613728,” Pixabay, August 18, 2018 available online here. The picture is used for illustration purposes only. The goat in the picture is not necessarily a dairy goat.

Geographic reference: United States Year: The year ended March 2021 Market size: $62 million

When one thinks of citrus fruit, oranges, grapefruit, or lemons may come to mind. Today’s market size shows the total U.S. sales of one type of orange, the Sumo Citrus, for the year ended March 2021. Sumo Citrus sales accounted for nearly 3% of the $2.1 billion citrus fruit market that year. Since March 2018, sales have grown 35% per year.

Sumo Citrus, the brand name in the United States, is a fairly new variety of mandarin orange.1 This fruit was first introduced in Japan in the 1970s and by the 1990s had become a popular, beloved fruit there. It’s a hybrid of navel oranges, pomelos, and mandarin oranges. After the U.S. government banned the seedlings for many years for fear they would spread plant viruses, Suntreat (now AC Brands) was finally given permission to grow the fruit about 20 years ago. The fruit was first sold in the United States in 2011.

Sumo Citrus’s popularity has grown since then, despite its high price. Sumo Citrus can cost 4 times as much as navel oranges. As a premium product that’s only in the season from January through April each year, the price may be seen as justified. In the United States, this fruit is only grown in the San Joaquin Valley in California. Sumo Citrus is difficult to grow. The skin is delicate, prone to sun damage. A clay-like substance is put over each fruit to protect it. Trees are hand-pruned. The fruit is hand-picked and hand-packed into each crate to make sure they don’t bruise. The trailers that transport the fruit to retailers are designed to provide a smooth ride to minimize damage in transit.

Why has this fruit become so popular? Perhaps it’s a combination of sweet taste, convenience (seedless, easily peeled), and marketing. While the short growing season can be seen as a disadvantage, AC Brands has turned it into a way to hype the fruit, encouraging consumers to buy the fruit while they can. Paid partnerships with social media influencers, ads in magazines, billboards in key markets, and prominent displays in supermarkets are other marketing strategies employed to influence consumers’ citrus buying habits.

1 The brand name was derived from the way the fruit looks. It’s a large fruit with a top knot, something like a sumo wrestler wears in the ring. In the United States, the brand name is synonymous with the name of the fruit itself.

Sources: Danielle Wiener-Bronner, “This Little-known Japanese Fruit Now Has a Cult Following,” CNN Business, March 31, 2021 available online here; “FAQs,” Sumo Citrus available online here; “The Farms,” Sumo Citrus available online here. Image source: Haruo, “File:Sumo (dekopon) supermarket display in Seattle.jpg,” Wikimedia Commons, February 25, 2016 available online here, CC BY-SA 4.0

July 13 is National French Fry Day. In a survey conducted by a San Francisco marketing agency, regular fries were the favorite of about a quarter of respondents, followed by curly fries, steak-cut fries, crinkle, waffle, and wedges.

Geographic reference: North America Year: 2018 and 2026 Market size: $7.8 billion and $9.9 billion, respectively

July 13 is National French Fry Day in the United States but most residents do not need an excuse to eat one of their favorite fried foods. Per capita, Americans eat an estimated 30 pounds of french fries per year. Today’s market size shows the total revenues for french fries in North America for 2018 and projected for 2026. The United States accounted for more than four-fifths of the North American market in 2018. Growth is expected due to the increasing consumption of convenience foods, fried foods, and fast foods. This growth will be tempered, however, by an increasingly health-conscious population. Fried foods are linked to obesity and cardiac problems. To appeal to these health-conscious consumers, companies have introduced low carbohydrate, air-fried, and baked varieties.

Frozen french fries dominated the market in 2018 and are expected to continue to do so through 2026. Revenues in this segment are also expected to experience the highest compound annual growth rate over this time period. Frozen french fries are easier to store and have a longer shelf life than the fresh-cut variety.

Consumers in the 20-35-year-old range accounted for the highest share of consumers in 2018. People of this age group tend to snack frequently and consume more fast food, packaged food, and ready-to-eat meals than other age cohorts mainly due to their busy lifestyles.

Quick-service restaurants held the highest market share in 2018, followed by other types of restaurants and institutions. The quick-service restaurant segment is expected to experience the highest compound annual growth rate through 2026 as more consumers prefer fresh food cooked in a short amount of time at an affordable price. In a survey conducted by Top, a marketing firm in San Francisco, consumers in the United States selected McDonald’s fries as their favorite, followed by Chick-fil-A, Five Guys, Wendy’s, and Arby’s.

To increase profitability and market share french fry manufacturers rely on new product launches, company acquisitions, and business expansion. Some major firms in the North American market (in alphabetical order) include Agristo NV, Alexia Foods, Aviko (Royal Cosun), Cavendish Farms, J.R. Simplot Co., Lamb Weston Holdings Inc., Luxfries BVBA, McCain Foods Ltd., Nathan’s Famous Inc., and Ore-Ida. McCain Foods produces one-third of the world’s french fries.

Sources: Sumesh Kumar and Roshan Deshmukh, “North America French Fries Market by Product (Regular and Frozen), Application (Below 18 Years, 20-35 Years Old, and Above 35 Years Old), and Distribution Channel (QSR, Institutional, Restaurants and Others): Opportunity Analysis and Industry Forecast, 2019-2026,” Allied Market Research Report Overview, January 2020 available online here; “North America French Fry Market Expected to Reach $9,948.3 Million in 2026,” Allied Market Research Press Release available online here; “National French Fry Day — July 13, 2021,” National Today available online here. Image source: StockSnap, “french-fries-salt-food-brown-food-923687,” Pixabay, September 4, 2015 available online here.

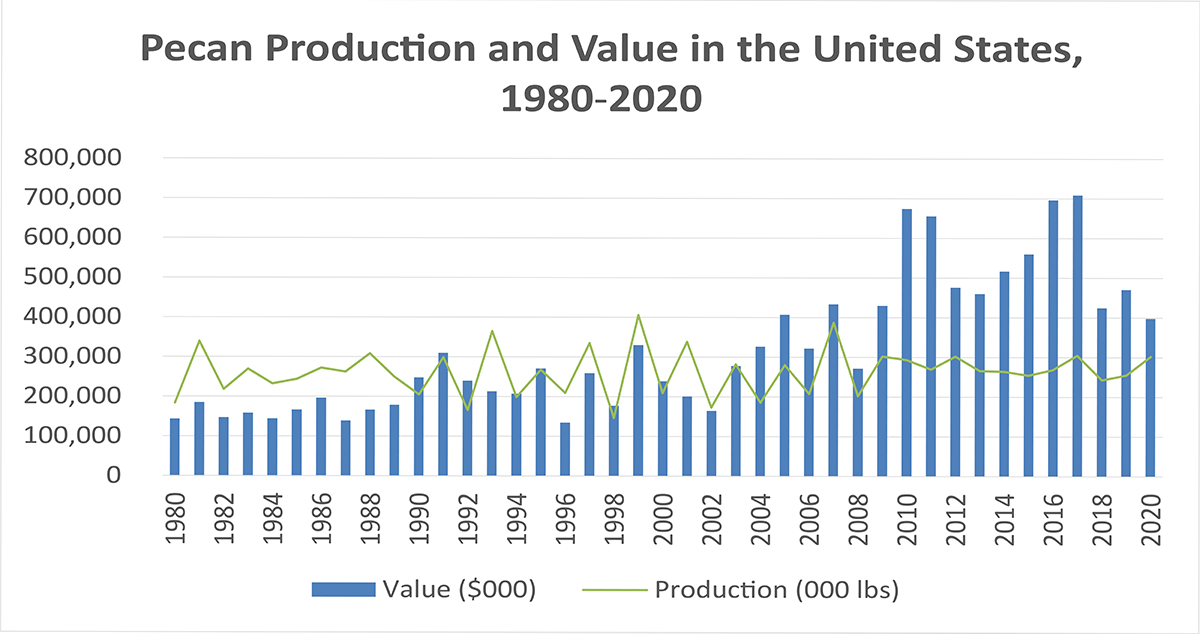

Geographic reference: United States Year: 1980, 1990, 2000, 2010 and 2020 Market size: $143.3 million, $247.6 million, $238.8 million, $674.8 million and $398.8 million, respectively

June 24th is National Pralines Day in the United States. A praline is a confection made of nuts and a sugary, caramelized coating. While the exact inspiration behind pralines is in doubt, what is certain is that it was named after a French sugar industrialist and diplomat from the early 17th century, César, duc de Choiseul, comte du Plessio-Praslin, whose personal chef, Clement Lassagne, invented the sugary treat. It’s believed that pralines were brought to the United States by the Ursuline nuns who came to New Orleans in 1727. The Ursuline nuns were in charge of young women who were sent from France at the request of the colonial governor of Louisiana and founder of New Orleans, Jean-Baptiste Le Moyne de Bienville, in order to marry colonists living in New Orleans. As part of their education, the women were taught “the art of praline making.”1 Pralines were originally made with almonds, but almonds were in short supply in Louisiana so cooks substituted pecans whose trees are native to the area. In the mid-to-late 19th century Pralinières were women who sold pralines on the streets of the French Quarter. This provided a source of income, without any strings attached, for free women of color.

Today’s market size shows the value of utilized pecan production in the United States from 1980 to 2020 in 10-year intervals. As the graph above shows, since 1980, production has varied widely from year to year, with the lowest and highest production falling in back-to-back years: 146.4 million pounds in 1998 and 406.1 million pounds in 1999. Since 2009, production has stabilized between about 245 million pounds and 302 million pounds. The value of production also varied during this time period but trended steadily upward until 2010 when the value of pecans reached its highest level in at least the past 30 years, a 57% increase from 2019. Over the next three years, the value of pecans dropped, with the biggest drop coming between 2011 and 2012.

From 2013 to 2017, the value of utilized production trended upward again, reaching a high of $709.4 million. 2017 was also the year with the highest utilized production since 2007 at almost 304.9 million pounds. Since then, the value has trended downward. From 2017 to 2018, utilized production dropped 27%, but has been climbing steadily ever since, reaching 302.4 million pounds in 2020. Production value, on the other hand, dropped 43.8% over this time period.

The fall in value from 2018 to 2020 from the 2017 high may be attributed, in part, to the trade war between China and the United States. Before the trade war, China was the largest export market for U.S. grown pecans. Chinese demand for pecans influenced the type of pecans growers produced, varieties of oversized nuts with high yields. Since the trade war began, Chinese demand for pecans grown in the United States dropped considerably, with prices falling in parallel. But consumer demand did not abate. Many of China’s pecan buyers have since turned to Mexico. Mexico’s exports to China increased by more than 3,000% in 2018 from a year earlier. Mexican pecans exported to China carry a 7% tariff. A tariff of 47% is applied to pecans from the United States.

Meanwhile, Mexican pecan growers have expanded their market into the U.S. and more U.S. buyers are buying. The United States is the largest export market for Mexican pecans. Because of lower production costs, pecans grown in Mexico are less expensive than pecans grown in the United States.2 According to Lanair Worsham, owner of Worsham Farms in Camilla, Georgia, and a member of the Georgia Pecan Commission, “If you eat a pecan product here in America, there’s a 75% chance that it’s Mexican.” Pecans from Mexico can be found in pies and other products on grocery store shelves and on restaurant menus.

Several officials, including the Georgia Agricultural Commissioner, lobbied during negotiations on the U.S.-Mexico-Canada Agreement to include a provision to make it easier for U.S. farmers to file anti-dumping and countervailing claims against exporters, but the provision was ultimately left out of the agreement. In 2020 some growers were worried about the challenges facing the U.S. pecan industry, especially in the southeast where growers were still recovering from hurricanes. Will the industry remain sustainable for the foreseeable future?

Mexico is the largest producer of pecans in the world, claiming 48% of the global supply. The United States follows with 46%. South Africa (4%) and Australia (1%) also produce pecans for the world market. In the United States, 15 states produce pecans commercially: Alabama, Arkansas, Arizona, California, Florida, Georgia, Kansas, Louisiana, Missouri, Mississippi, North Carolina, New Mexico, Oklahoma, South Carolina, and Texas. Georgia produced the most in 2020, 142 million pounds, followed by New Mexico (77 million) and Texas (45.4 million). There are more than 1,000 varieties of pecans, many named after Native American tribes. Only 20 varieties are produced commercially, the most popular being Cape Fear, Desirable, Moreland, Stuart, and Natives. Natives are wild seedlings. Wild varieties tend to have thicker shells and less nutmeat. Improved varieties have thinner shells that can be broken by hand and have more nutmeat. Improved varieties are preferred for commercial use.

1 Source: “History of the Praline,” Southern Candymakers available online here. 2 Production costs in Mexico are approximately $860 per acre. In the southeastern United States, $1,500 per acre.

Sources: “Tree Nuts,” Fruit and Tree Nuts Yearbook Tables, Economic Research Service, United States Department of Agriculture, October 29, 2020 available online here; “History of the Praline,” Southern Candymakers available online here; “Pecan Production,” National Agricultural Statistical Service, Agricultural Statistics Board, United States Department of Agriculture, January 21, 2021 available online here; “What are the Differences in Pecan Varieties?” Royalty Pecan Farms, December 1, 2014 available online here; Matthew Bailey, “Pecan Prices and Trade Tensions Between China and the US,” Pecan Report, July 23, 2020 available online here; Clint Thompson, “Georgia Pecan Grower: Industry on Brink of Collapse,” VSCNews, November 20, 2020 available online here; “3000% Increase in Mexican Pecan Exports to China,” Produce Report, August 12, 2019 available online here; Bill Tomson, “Georgia’s Pecan and Blueberry Farmers Plead for Protection from Mexico,” Agri-Pulse, August 19, 2020 available online here; Clint Thompson, “Southeast Pecan Industry Continues to Face Challenges,” VSCNews, February 14, 2020 available online here; “History of Pecans,” U.S. Pecan Growers Council available online here; “How Pecans are Grown,” U.S. Pecan Growers Council available online here; “Jean-Baptiste Le Moyne de Bienville,” Encyclopedia Britannica, March 2, 2021 available online here. Image source: Graph was created in-house from the data in “Tree Nuts,” Fruit and Tree Nuts Yearbook Tables, October 29, 2020 available online here and “Pecan Production,” National Agricultural Statistical Service, Agricultural Statistics Board, United States Department of Agriculture, January 21, 2021 available online here.

Geographic reference: United States Year: 2017, 2018, and 2019 Market size: $599.9 million, $511.2 million, and $518.9 million, respectively

In the United States, April 13th is National Peach Cobbler Day. The day was invented in the 1950s by the Georgia Peach Council in order to sell more canned peaches. However, dessert cobblers have been around since the 19th century. These dishes were invented by settlers as they traveled westward in the early 1800s. Pies were popular among English and Dutch immigrants and fruit was readily available in the Eastern United States, but not having the ingredients and the ability to properly bake a pie as they traveled westward, settlers made do with what they had: fruit of some sort (preserved, canned, or dried) and biscuit dough. The ingredients were cobbled together in a Dutch oven and baked over an open fire until the dough was golden brown. The dish was eaten as breakfast or as a first or main course then. In the late 19th century, the cobbler was officially declared a dessert.

Today’s market size shows the value of utilized peach production in the United States in 2017, 2018, and 2019. In these years, production totaled 694,220; 638,020; and 658,830 tons, respectively. Since 2017, fewer peaches produced have gone to the fresh market. Processed peaches have increased their share of the market from 54.7% of the utilized crop in 2017 to 60.1% in 2019.

By far, California was the top state in terms of production, 495,000 tons, in 2019, with 53.1% being the clingstone variety. South Carolina was second with 63,700 tons, followed by Georgia (33,780 tons), Pennsylvania (19,080), New Jersey (17,980), Colorado (13,300), Washington (11,040), and Michigan (4,800).1 Top peach producers in the United States include Titan Farms and J.W. Yonce and Sons in South Carolina and Taylor Orchards, Dixie Bell Orchards, Lane Southern Orchards, and Pearson Farm in Georgia.2

Worldwide, the production of peaches (and nectarines) totaled 25.7 million tons in 2019. China produced the most, 15.8 million tons, or 61% of world production.3 Spain ranked second in production with 1.5 million tons, followed by Italy (1.2 million), Greece (926,620), and Turkey (830,057). The United States ranked 6th, producing 739,900 tons of peaches and nectarines.

1 Starting in 2018, estimates were discontinued for 12 of the 20 states the National Agricultural Statistical Service tracked previously. These states include, in order of 2017 utilized production, West Virginia, Illinois, Idaho, New York, Ohio, Maryland, Virginia, Utah, Texas, Missouri, North Carolina, and Alabama. 2 Source: Christina Herrick, “American and Western Fruit Grower’s 2014 Top Stone Fruit Growers,” Growing Produce, September 13, 2014 available online here. Most recent data available. The source gives a ranking of the top 25 stone fruit growers in the United States. Data used in this market size post are for stone fruit growers whose only stone fruit crop is peaches. 3 Source: “FAOSTAT: Crops,” Food and Agriculture Organization of the United Nations available online here. Data were downloaded on February 23, 2021. The source reports data for both peaches and nectarines combined. Peaches and nectarines are almost identical genetically. Peaches have a dominant gene variant that causes them to have a fuzzy coating. Nectarines have a recessive gene that causes their smooth skin.

Sources: “Noncitrus Fruits and Nuts 2019 Summary,” United States Department of Agriculture, National Agricultural Statistical Service, May 2020 available online here; Alexia Wulff, “A Brief History of Peach Cobbler,” Culture Trip, November 23, 2016 available online here; “FAOSTAT: Crops,” Food and Agriculture Organization of the United Nations available online here; Christina Herrick, “American and Western Fruit Grower’s 2014 Top Stone Fruit Growers,” Growing Produce, September 13, 2014 available online here; Christine Gallary, “What’s the Difference Between Peaches and Nectarines?” Kitchn, July 20, 2015 available online here. Image source: Flockine, “peach-fruit-fruits-peach-tree-bio-2632182,” Pixabay, August 11, 2017 available online here.

Geographic reference: World Year: 2018 and 2026 Market size: $2.53 billion and $6.22 billion, respectively.

“Have you ever pondered the miracle of popcorn? It starts out as a tiny, little, compact kernel with magic trapped inside that when agitated, bursts to create something marvelously desirable. It’s sort of like those tiny, little thoughts trapped inside an author’s head that―in an excited explosion of words―suddenly become a captivating fairy tale!”

— Richelle E. Goodrich

Whether it’s buttered and salted, caramel-coated, or tossed with spicy buffalo sauce seasoning, popcorn is a favorite snack among those who are looking to indulge their cravings as well as those looking for better-for-you, healthier snack options. While certain coatings may negate some of its healthful benefits, popcorn contains concentrated sources of fiber, polyphenolic compounds, vitamin B complex, antioxidants, and assorted proteins. Air-popped popcorn has 31 calories per cup; oil-popped 55. Today’s market size shows the global revenues for ready-to-eat popcorn in 2018 and projected for 2026.

Many scholars agree that popcorn originated in the Americas. The oldest ears of popcorn ever found were discovered in a bat cave in west-central New Mexico in 1948. They are estimated to be 5,600 years old. Early North American explorers noticed Native Americans not only eating popcorn but also using it in necklaces and headdresses. European settlers ate popcorn as a breakfast food with milk or cream. During the Great Depression, popcorn became popular as a low-cost snack and with most of the supply of sugar used for the war effort, popcorn became an alternative to sugary snacks during World War II.

Popcorn comes in two shapes: snowflake (or butterfly) and mushroom. The snowflake variety is larger and is the type sold in movie theaters, ballparks, and other entertainment venues. The snowflake variety is also the type people buy to pop at home. The mushroom variety is more compact and used in bagged snacks and in candy confections because it doesn’t crumble.

In 2017, the last year for which data exist, there were 1,051 popcorn farms in the United States spanning more than 221,000 acres. In comparison, there were 304,801 farms (84.7 million acres) that grow corn for grain and 20,784 sweet corn farms (496,096 acres). Popcorn is grown in most states, with Nebraska harvesting the most crop, 368.62 million pounds shelled, in 2017. Indiana (352.39 million), Ohio (129.76 million), Illinois (93.29 million), and Missouri (46.84 million) round out the top 5 states. Together, they represent 92.5% of popcorn harvested that year. Almost all popcorn production in the U.S. is contracted with processors. Leading global ready-to-eat popcorn manufacturers include The Hershey Company, Conagra Brands Inc., Snyder’s-Lance Inc., Intersnack Group GmbH & Co. KG, PepsiCo, Eagle Family Foods Group LLC, Propercorn, Quinn Foods LLC, The Hain Celestial Group Inc., and Weaver Popcorn Company Inc.

Most of the popcorn consumed around the world is produced in the United States but popcorn is also grown in other parts of North America, South America, Europe, Australia, and South Africa. More than 80% of popcorn produced in the U.S. is consumed domestically. In the ready-to-eat segment, North America held 31.23% of the market in 2018. Consumers’ preference for convenience and a variety of flavors will spur demand through at least 2026. In the United Kingdom, 90% of popcorn sold in supermarkets is ready-to-eat, with most of the kernels sourced from the U.S., France, and Italy and then popped in the UK. The Asia-Pacific region’s market share is expected to increase the fastest over this time period as a growing preference for this type of snack and greater awareness of popcorn’s health benefits will create higher demand in the region.

In 2018, the household segment claimed 53.23% of the market; commercial claimed the rest. With health departments shuttering movie theaters and other entertainment venues because of the coronavirus pandemic, the household segment is expected to dominate the market in 2020. In the United States, the ready-to-eat popcorn segment1 at retail amounted to $1.49 billion of the overall $26.7 billion salty snack market in the 52 weeks ended May 17, 2020, a 5% increase from the same period a year before. Although sales have been increasing in the last 5 years, the increases have been getting smaller. In 2015, this segment’s sales increased by 18.17%; In 2019, 4.1%. While the ready-to-eat segment has been increasing, the microwave segment has been declining year over year. Except in 2020. After declining an average of 3.39% from 2015 to 2019, sales jumped 13.3% in 2020 as more people stayed home with their families and binged watched favorite movies and TV shows. Raw kernel sales also saw a spike in sales. The convenience of ready-to-eat popcorn, which many may have reached for when life was busier, was eclipsed by the comfort of warm, home-popped, buttery (or sweet and savory) popcorn as people’s lifestyles slowed down dramatically.

1 Includes caramel corn.

Sources: “Global Ready-to-Eat Popcorn Market is Expected to Reach USD 6.22 Billion by 2026: Fior Markets,” GlobeNewswire, March 3, 2020 available online here; 2017 Census of Agriculture, United States Department of Agriculture, National Agricultural Statistics Service, April 2019 available online here; “Popcorn Statistics and Facts,” See California available online here; Romy Schafer, “Ready to Eat Popcorn Thrives: State of the Industry 2015,” Snack Food & Wholesale Bakery, July 15, 2015 available online here; Douglas J. Peckenpaugh, “Snack Market Overview: State of the Industry 2016,” Snack Food & Wholesale Bakery, July 11, 2016 available online here; Liz Parker, “State of the Industry 2017: Popcorn Offers More Choices for Consumers,” Snack Food & Wholesale Bakery, July 18, 2017 available online here; Melissa Kvidahl Reilly, “State of the Industry 2018: Ready-to-Eat Popcorn Tops Other Varieties,” Snack Food & Wholesale Bakery, July 17, 2018 available online here; Ed Finkel, “State of the Industry 2019: Popcorn Delivers on Healthy and Indulgent Options,” Snack Food & Wholesale Bakery, July 19, 2019 available online here; Ed Finkel, “State of the Industry 2020: Popcorn Sales Explode,” Snack Food & Wholesale Bakery, July 17, 2020 available online here; “Popcorn Profile,” United States Department of Agriculture, Agricultural Marketing Resource Center, October 2018 available online here; “Popcorn: Ingrained in America’s Agricultural History,” United States Department of Agriculture, National Agricultural Library, Special Collections Exhibits available online here; “Popcorn Facts,” Popcorn Boss available online here; Key Facts About Popcorn in the UK,” SNACMA available online here; John Balint, “Popcorn 101: Butterflies, Snowflakes & Mushrooms (Oh My!),” Popcornopolis, November 11, 2015 available online here; “Popcorn Quotes,” Goodreads available online here; Image source: John R Perry, “popcorn-candy-food-sweet-dessert-463660,” Pixabay, October 8, 2014 available online here. Use of image does not constitute an endorsement.

Geographic reference: World Year: 2019 and 2027 Market size: $4.69 billion and $10.23 billion, respectively

“Salad can get a bad rap. People think of bland and watery iceberg lettuce, but in fact, salads are an art form, from the simplest rendition to a colorful kitchen-sink approach.”

— Marcus Samuelsson

After a long weekend of eating turkey, mashed potatoes and gravy, stuffing, green bean casserole, pumpkin pie, and assorted other goodies, are you craving something lighter and healthier? A salad perhaps?

Today’s market size shows global revenues for packaged salad in 2019 and projected for 2027. Packaged salads were first introduced in 1986. At first, they mostly contained bite-sized pieces of iceberg lettuce and perhaps some shredded carrots, onions, and cheese. These products didn’t catch on with consumers until the mid-2000s when companies began adding a variety of greens such as arugula, baby spinach, and baby kale to their product offerings. More recently, companies have been including ingredients such as broccoli, cauliflower, peapods, avocado, almonds, pecans, and cranberries. Vegetarian packaged salad claimed 65% of revenues in 2019, but non-vegetarian revenues are expected to grow the fastest, at a compound annual growth rate (CAGR) of 10.5%, between 2020 and 2027 as companies add a variety of meats and seafood to their salad kits to appeal to a wide audience, from chicken, ham, and bacon to shrimp, salmon, and squid.

As with other sectors of the food and beverage industry, the growing number of health-conscious consumers are contributing to growth in this segment also. In addition, packaged salads offer time-saving convenience for those who have little time to prepare healthy meals at home. Those shopping for organic produce have created a sizeable market for these products too. While the conventional segment constituted more than 70% of revenues in 2019, the organic segment is expected to grow the fastest through 2027 as demand for organic packaged food in general at both the consumer and commercial levels has increased, especially in Europe and North America. In the United States in 2019 organic produce revenues at retail set a record high of $5.8 billion, with almost 20% of organic produce sales coming from packaged salads. Millennials, especially, prefer packaged to pick-your-own produce. According to the Food Industry Association, “shoppers have the highest interest in nutrition and origin information, and preparation/storage instructions.”

More than 80% of packaged salads are bought offline at supermarkets and warehouse clubs, but online sales are expected to grow the fastest through 2027 as e-commerce and grocery delivery become more popular. Sales from traditional online retailers such as Amazon, along with e-commerce sales from supermarkets, grocery delivery firms, and direct sales from packaged salad firms are expected to grow at a CAGR of 11% over this time period. The North American region claimed 35% of revenues in 2019. The growing demand in the region has spurred companies to introduce new gourmet, restaurant-inspired products to the market. New product launches appealing to a variety of tastes has increased global sales over the past few years. The Asia-Pacific region is expected to experience the fastest growth in the next several years as more Millennial and Generation Z consumers seek out healthier food choices. Some prominent companies in the packaged salad market include BrightFarms, Dole Food Company Inc., Earthbound Farm, Eat Smart, Fresh Express, Garden Life, Gotham Greens, Mann’s, Misionero, and Bonduelle.

Sources: “Packaged Salad Market Size, Share & Trends Analysis Report by Product (Vegetarian, Non-vegetarian), by Processing (Organic, Conventional), by Distribution Channel, by Region, and Segment Forecasts, 2020 – 2027,” Grand View Research Report Overview, July 2020 available online here; “Packaged Salad Market Size Worth $10.23 Billion by

2027 | CAGR: 10.2%: Grand View Research, Inc.,” CISION PR Newswire, November 12, 2020 available online here; Keith Loria, “Produce Profits are in the Bag,” Supermarket News, March 21, 2019 available online here; Mary Ellen Shoup, “Organic Produce Sees Record Sales in 2019: ‘Packaged Salads are the Single Largest Driver of Organic Dollars’,” Food Navigator-USA.com, January 21, 2020 available online here; “Salad Quotes,” BrainyQuote available online here. Image source: Michael Moriarty, “salad-food-dish-plate-meal-2150548,” Pixabay, March 21, 2017 available online here.

More than 200 varieties of potatoes are grown in the United States.

Geographic reference: United States Year: 2018, 2019, 2020 Market size: $11.5 billion, $11.7 billion, and $13.0 billion, respectively

“Not everyone can be a truffle. Most of us are potatoes. And a potato is a very good thing to be.”

— Massimo Bottura, Massimo Bottura: Never Trust a Skinny Italian Chef

Despite Thanksgiving looking quite different this year due to the pandemic — minimal travel, smaller family gatherings, perhaps a smaller turkey too — there’s a good chance that whether mashed, baked, boiled, or fried, potatoes will still be on the menu.

Today’s market size shows total retail sales of potatoes for marketing years (MY) 2018 to 2020, July to June, in the United States. Figures include sales at supermarkets, drug stores, mass merchandisers, military commissaries, and select club and dollar chains. According to the U.S. Department of Agriculture, the United States produced 40.6 billion pounds of potatoes in 2019. More than 200 varieties are grown in the U.S. These varieties fall into 7 categories: russet, red, yellow, white, blue/purple, fingerling, and petite. Russets are the most preferred potato in the U.S. Potato production occurs in most states with Idaho producing the most in 2019, 15.9 billion pounds, followed by Washington (11.6 billion), Wisconsin (3.2 billion), Oregon (2.8 billion), and North Dakota (2.3 billion). A majority of potato farms in the United States are family-owned, including R.D. Offutt Farms, the largest potato grower in the United States. R.D. Offutt Farms operates farms in seven states growing more than 50,000 acres of potatoes annually.

Most potatoes bought at retail, however, have been processed in some way. For MY 2020, potato chips took the highest share in terms of volume (37%). Fresh potatoes followed with a 31% share and frozen rounded out the top 3 with a 17% share. In terms of dollar sales, potato chips garnered the top spot with $6.3 billion in sales, followed by fresh ($3.3 billion), and frozen ($1.9 billion). Sales for all retail categories of potatoes, except deli prepared sides, increased from the previous year. Many categories increased by double-digits. By volume, frozen potato sales increased the most, 15.3%; by value, dehydrated did (22.1%). Fresh potatoes increased 9.5% and 14.7%, respectively.

The United States also exports and imports potatoes. Exports totaled 7.7 billion pounds and imports totaled 6.1 billion pounds in 2019. The United States ranked sixth in the world among top raw potato exporters and importers. The U.S. exported the most potato products to Japan, $365 million worth. Potato products from the U.S. account for nearly 70% of Japan’s total potato product imports annually. Besides Japan, Canada, Mexico, the Philippines, and South Korea are top markets for U.S. potatoes. By fresh weight equivalent, frozen potatoes constituted more than half (51%) of exports during MY 2020, followed by dehydrated (27%), fresh (15%), potato chips (6%), and seed potatoes (1%). Because of reduced demand in the foodservice sector due to the coronavirus pandemic, total exports fell 2.2% (-2.6% by value) from the previous year. However, the drop in exports did not affect all categories. Dehydrated potato export volume rose by 1% over this time period. Sizeable decreases in exports to Thailand, the Philippines, Taiwan, and Central America were offset by significant increases in exports to the European Union, northern Africa, the Middle East, and South Korea.

By weight, more than 60% of potato product imports to the U.S. in 2019 were frozen French fries and potatoes. Fresh potatoes garnered 21.1% of total imports. Potato starch (8.0%), dehydrated potatoes (5.0%), seed potatoes (4.0%), and potato chips (1.5%) constituted the remaining. Despite a decline in demand from the foodservice sector due to the coronavirus restrictions from April to June 2020, imports increased 8% from MY 2019 to MY 2020. Dehydrated potato imports increased the most, 24%, followed by fresh potatoes (10%), potato chips (7%), and frozen and seed potatoes (1% each). Nearly 100% of fresh potato imports came from Canada, as did seed potatoes. Canada also imported the most frozen French fries and potatoes and potato chips. Most dehydrated potatoes came from Mexico. Most imported potato starch came from the Netherlands.

Sources: “Total Potato Sales: Marketing Year 2020,” Potatoes USA available online here; Daniel Workman, “Potatoes Exports by Country,” World’s Top Exports, July 6, 2020 available online here; Daniel Workman, “Potatoes Imports by Country,” World’s Top Exports, May 1, 2020 available online here; Annual Potato Yearbook, National Potato Council, 2020 available online here; “U.S. Imports of Potato Products Summary,” Potatoes USA, February 2020 available online here; “Food Availability (Per Capita) Data System,” United States Department of Agriculture, Economic Research Service, September 23, 2020 available online here; “Report: The US Dominates Japan’s Total Potato Product Imports,” Potato News Today, February 12, 2020 available online here; John Toaspern, “Dealing With Disruption,” Potato Grower, November 2020, page 37 available online here; “R.D. Offutt Company,” PotatoPro, October 15, 2013 available online here; “U.S. Potato Industry: U.S. Grower Profiles,” Potatoes USA available online here; “R.D. Offutt Company’s Proud Local History” available online here; M. Shahbandeh, “Preferred Potato Varieties in the U.S. 2019,” Statista, June 10, 2020 available online here; “Potato Types,” Potatoes USA available online here. Original source: IRI Image source: Andreas Böhm, “potatoes-harvest-autumn-color-3783878,” Pixabay, November 1, 2018 available online here.

Flowers of the cuminum cyminum (cumin) plant. Cumin is the most popular spice in the world.

Geographic reference: World Year: 2019 and 2027 Market size: $5.86 billion and $9.70 billion, respectively

I went into the garden in the morning dusk,

When sorrow enveloped me like a cloud;

And the breeze brought to my nostril the odor of spices,

As balm of healing for a sick soul.

— Moses ibn Ezra

What comes to mind when you hear the word “spice”? In autumn, the first thing that may come to mind is “pumpkin spice” and the warmth of cinnamon, nutmeg, ginger, cloves, and allspice. The smell of spices can be evocative, bringing back memories of a place visited, a beloved family recipe, or a special meal enjoyed with friends and family around the dinner table. Today’s market size shows worldwide revenues for spices in 2019 and projected for 2027.

Spices have been used as far back as 5000 B.C.E. Throughout the millennia they’ve been used as medicine and to promote health as well as to flavor and preserve food. They’ve been highly valued as trade goods for thousands of years. The spice trade developed around 2000 B.C.E. on the Indian subcontinent with cinnamon and pepper and in East Asia with herbs and pepper. Egyptians used spices for embalming. Their demand for exotic herbs and spices helped fuel global trade. Alexandria became the main trading center as Indonesian merchants traveled around China, India, the Middle East, and the east coast of Africa and Arab merchants traveled through the Middle East and India.

During the Middle Ages, spices were among the most expensive and highly demanded products in Europe. They became status symbols and signs of luxury among the wealthiest citizens. Spiced wine was popular. The most common spices in demand were black pepper, cinnamon, cumin, nutmeg, ginger, and cloves. Explorers to the New World brought back allspice, capsicum peppers, and vanilla. By 1700, the importance of spices began to wane as Europeans preferred coffee, chocolate, and tobacco. The United States entered the spice trade in the latter part of the 18th-century trading salmon, codfish, tobacco products, flour, soap, candles, butter, cheese, and beef for spices. Salem, Massachusetts profited tremendously from the Sumatra pepper trade. Most of the pepper was re-exported to Europe or sent for processing and distribution to Philadelphia, Boston, and Baltimore. By the mid-1800s an overproduction of spices and the Civil War brought an end to the pepper trade. More recently, pepper shortages have raised prices in many parts of the world.

Spices are seeds, dried fruits, roots, and barks. They’re mostly used to add flavor, aroma, and color to foods. They’re also used in medicines, dyes, cosmetics, and perfumes. The most popular spice in the world is cumin. In the United States, cinnamon, ginger, and black pepper are the most popular. Powdered spices claimed more than 50% of global revenues in 2019 owing to their versatility and long shelf life. They also don’t have to be refrigerated. However, increasingly consumers are preferring whole spices to provide fresher flavors to their food. This segment of the market is expected to grow the fastest from 2020 to 2027. There has been a rising demand for ready-to-cook spice mixes also both for home use and in the foodservice industry. These save busy consumers time when preparing meals at home and provide a consistent flavor profile in recipes. Newer mixes that provide aromatic and fusion flavors are becoming more popular as people seek out more exotic foods. Demand for spices is also expected to increase as spice manufacturers advertise on social media platforms such as Facebook, Pinterest, and Twitter encouraging people to try various spices in recipes at home.

Many spices have antioxidants, substances that protect cells from damage. Some doctors and dietitians advocate adding spices to one’s diet to get added health benefits. Some people incorporate cinnamon into their diet to lower blood pressure, turmeric to fight inflammation, ginger to relieve nausea, cayenne (capsaicin) to ease pain, cumin to boost the immune system, and garlic for heart health and to lower cholesterol and triglycerides. In traditional medicine, black cumin has been used to treat asthma, diabetes, hypertension, fever, inflammation, bronchitis, dizziness, eczema, and gastrointestinal disturbances.

Studies on the health effects of spices generally focus on spices in the form of supplements although some doctors caution against taking commercial spice supplements that have not been independently verified by a third-party organization because they’re not regulated and may not contain what they say they do. Several spices are currently being investigated in preclinical, clinical, and therapeutic trials as new treatments for several diseases, including cancer. Perhaps in the future new spice-based drugs will be developed.

The Asia Pacific region is a leading producer and exporter of spices garnering more than a 35% revenue share in 2019. Most spices are grown in India, Vietnam, China, and Thailand, with China being one of the largest consumers of spices in the region. Over the last few years, Indian spices have seen a surge in demand worldwide. Leading spice manufacturers include Ajinomoto Co. Inc., Associated British Foods plc, Ariake Japan Co. Ltd., Baria Pepper, Kerry Group, The Bart Ingredients Co. Ltd., DS Group, Everest Spices, Dohler Group, and McCormick & Company Inc.

Sources: “Spices Market Size, Share & Trends Analysis Report by Product (Pepper, Turmeric), by Form (Powder, Whole, Chopped & Crushed), by Region (North America, Europe, APAC, CSA, MEA), and Segment Forecasts, 2020 – 2027,” Grand View Research Report Summary, October 2020 available online here; “Spices Market Size Worth $9.70 Billion by 2027 | CAGR: 6.5%: Grand View Research, Inc.,” CISION PR Newswire, October 12, 2020 available online here; “Spice,” Wikipedia, October 13, 2020 available online here; “The Most Used Herbs Across the Globe,” Urban Cultivator available online here; “History of the Spice Trade,” History & Special Collections, UCLA Louise M. Darling Biomedical Library, 2002 available online here; Alexander Yashin, Yakov Yashin, Xiaoyan Xia, and Boris Nemzer, “Antioxidant Activity of Spices and Their Impact on Human Health: A Review,” Antioxidants, September 15, 2017 available online here; “5 Spices With Healthy Benefits,” Johns Hopkins Medicine available online here; Krishnapura Srinivasan, “Cumin (Cuminum cyminum) and Black Cumin (Nigella Sativa) Seeds: Traditional Uses, Chemical Constituents, and Nutraceutical Effects,” Food Quality and Safety, Oxford Academic, March 2018 available online here; “Seasoning and Spices Market Size, Share & Trends Analysis Report by Product (Herbs, Salt & Salts Substitutes, Spices), by Application, by Region, and Segment Forecasts, 2020 – 2027,” Grand View Research Report Summary, July 2020 available online here. Image source: Herbolario Allium, “Cuminum cyminum,” Wikimedia Commons, May 1, 2012, available online here. Creative Commons License CC BY 2.0.

Mozzarella is the top-selling type of vegan cheese.

Geographic reference: World Year: 2019 and 2027 Market size: $1.01 billion and $2.66 billion, respectively

Today’s market size shows the global revenues for vegan cheese in 2019 and projected for 2027. The global vegan cheese market is a very small fraction of the $69.7 billion dairy cheese market, however, due to the increasing popularity of vegan cheese revenues are expected to more than double by 2027, growing at a compound annual growth rate (CAGR) of 12.8% from 2020 to 2027. Demand is increasing for all plant-based foods including vegan cheese. Veganism is more common among consumers, either as a health choice or in response to concern for animal welfare and the environment. But vegan cheese is not just in demand among vegans. Flexitarians seek out plant-based alternatives in order to reduce the amount of meat and dairy in their diets. And, according to the U.S. National Institutes of Health, 65% of the global population has trouble digesting lactose, the sugar found in dairy products. Substituting vegan cheese for dairy cheese in many recipes allows this population the ability to enjoy foods they might not be able to eat otherwise.

Vegan cheese made with cashews held the largest share of the market at 35%. Products made with soy are expected to gain market share through at least 2027. Soy is a low-cost dairy alternative and is low in cholesterol with other health benefits. By type, mozzarella held the highest share at 30%, followed by Cheddar, cream cheese, and parmesan. Vegan mozzarella is in high demand in western countries where Italian food, including pizza, are popular. Ricotta-style vegan cheese is expected to see the fastest growth as more popular recipes incorporate this ingredient in appetizers, pizza toppings, and desserts.

With the increasing consumer demand for plant-based cheese, these products are no longer relegated to health food stores and specialty grocers. Increasingly supermarkets and convenience stores are stocking these products. More than 50% of vegan cheese is consumed in the household. Growth in this segment is due to higher availability and a willingness by consumers to pay for premium products. The foodservice segment of the market is expected to see the fastest growth as more restaurants, fast-food chains, and casual-dining establishments add plant-based offerings to their menus. The growing popularity of vegan meal kit services will also contribute to the growth in vegan cheese sales. Plant-based meal kits by Allplants Ltd. have been so popular in the United Kingdom, the company plans to expand to other parts of Europe and North America. Europe accounted for a 40% share of global vegan cheese revenues, the highest in the world, with the United Kingdom and Germany being the major markets in the region. The Asia-Pacific region is expected to experience the fastest CAGR, 14.3%, from 2020 to 2027.

In the United States, brands such as Daiya, Follow Your Heart, Kite Hill, Violife, and Go Veggie, whose companies exclusively create vegan and vegetarian food items, have seen top 10 sales in 2020. Of the top 5 processed/imitation shredded cheese brands, 4 were vegan/vegetarian brands. Kraft Velveeta claimed the top spot with sales of $9.9 million, followed by Daiya ($8.8 million), Follow Your Heart ($2.5 million), Violife ($1.3 million), and Go Veggie ($1.1 million). In the processed/imitation sliced cheese category Daiya and Follow Your Heart ranked 8 and 10 respectively. In the soft cream cheese category, Kite Hill was the third-ranked brand (excl. Private label) with sales of $2.5 million, above Crystal Farms and Kraft. Tofutti and Daiya ranked sixth and seventh, respectively.1

To capitalize on the growing popularity of plant-based foods, some established dairy firms are including plant-based dairy items in their portfolios, either by acquiring companies with plant-based brands or developing products in house. In 2018, Miyoko’s joined Nestlé-backed accelerator Terra and has been working with the company to craft plant-based cheese and butter by combining proprietary technology and age-old creamery methods. In September 2019 Kraft Heinz provided seed funding for San Francisco-based animal-free cheese company New Culture. Before that, in September 2017, J Sainsbury PLC created vegan cheese products under its private label brand to sell in its Sainsbury’s supermarkets in the United Kingdom. As Dominic Borrelli, President of Plant-Based Food and Beverages and Premium Dairy at Danone North America states: “Overall, consumers are recognizing dairy-free doesn’t only need to be for those with allergens or those practicing a dairy-free lifestyle but can simply be enjoyed because it’s delicious!”

1 Ranking and sales data for processed/imitation cheese are for the 12 weeks ended March 22, 2020. Ranking and sales data for soft cream cheese are for the 12 weeks ended April 19, 2020. All data are originally from IRI, a market research firm, and can be found in Frozen & Refrigerated Buyer. See source note for more information.

Sources: “Vegan Cheese Market Size, Share & Trends Analysis Report by Product (Mozzarella, Cheddar, Parmesan, Ricotta, Cream), by Source (Cashew, Soy), by End-use (Household, Foodservice), by Region, and Segment Forecasts, 2020 – 2027,” Grand View Research Report Summary, September 2020 available online here; “Vegan Cheese Market Size Worth $2.66 Billion by 2027 | CAGR: 12.8%: Grand View Research, Inc.,” CISION PR Newswire, September 15, 2020 available online here; “Market Value of Cheese Worldwide from 2019 to 2025,” Statista.com available online here; Frozen & Refrigerated Buyer, May 2020, pp. 10-12 available online here; Frozen & Refrigerated Buyer, June 2020, p. 12 available online here; Brian Kateman, “Plant-Based Meal Kits and Delivery Services are on the Rise,” Forbes, December 11, 2019 available online here; Andy Coyne, “Plant-based Priorities — Dairy Companies with a Stake in Dairy-free,” just-food, August 4, 2020 available online here; Andy Coyne, “Nestlé-backed U.S. Accelerator Terra Reveals Latest Cohort,” just-food, October 4, 2018 available online here; “Danone: ‘The Emphasis on Plant-Based Nutrition Will Accelerate Over Time & We Are Here to Help Meet Those Needs,'” Vegconomist, May 6, 2020 available online here. Image source: Amber Engle, “Rainbow Veggie Pizza Slice,” Unsplash, July 25, 2020 available online here.

Extruded snacks are processed food products made from a combination of ingredients that are either pushed through a mold or precision cut. Extrusion allows for mass food production and uniformity of the final product. Extruded snacks are produced from starches — potatoes, rice, corn, tapioca, mixed grains, and others — and are high in calories and fat with low protein and fiber content. Some brands include Cheetos, SunChips, Goldfish® crackers, and Fritos corn chips. In general, extruded snacks are perceived as being unhealthy. However, in recent years, in response to consumer preferences for better-for-you snacks, manufacturers have been incorporating healthier ingredients such as peas, lentils, chickpeas, cauliflower, and other vegetables into their products.

The extrusion process is also used to create nutrient-dense, shelf-stable snacks to combat malnutrition around the world. More than 200 million children under the age of 5 suffer from undernutrition,1 which is linked to 45% of deaths of children in this age group worldwide. In Cambodia, Nutrix, a tube-shaped wafer snack with a slightly sweet, slightly savory fish-based filling is used to combat malnutrition in that country. Previously, the Cambodian government relied on an imported nutrient-rich mix of milk powder, wheat flour, oat flour, and soy-protein as a therapeutic food. However, when prepared, this food became chewy and hard to swallow. Nutrix, on the other hand, is similar to a well-known local snack called Num Phom, uses local ingredients, and is more palatable. Children love it according to Lyndon Paul, co-founder of Danish Care Foods, manufacturer of Nutrix, and former product designer with Vissot, a local health food company.2 Since 2019, the private sector, non-governmental organizations, development agencies, and governments in Laos, Indonesia, Nepal, Bangladesh, and India have been interested in setting up Nutrix production facilities so that they can support malnutrition programs in their respective countries.

Today’s market size shows global extruded snack revenues for 2019 and projected for 2027. People are snacking more than they have in the past. In the United States, 95% of adults snack at least once a day, with 70% snacking two or more times a day. Many are foregoing entire meals and instead are snacking throughout the day. Consumers with busy lives who are looking for convenient, on-the-go, ready-to-eat foods to satisfy their hunger will contribute to the growing demand for extruded snacks over this time period. Health-conscious snackers will contribute to the growing demand for healthier ingredients in their favorite snack foods. Increasing attendance at entertainment venues, theaters, and other gathering places is expected to spur demand for these types of snacks at these sites. However, with governments throughout the world shutting businesses and imposing stay-at-home orders to slow the spread of COVID-19 in 2019 and 2020, demand for extruded snacks away from home are expected to decrease in the near future. Meanwhile, consumers are stocking up on shelf-stable, processed foods during the quarantine, including extruded snack foods. In an April 2020 Harris poll, 40% of those surveyed said they’ve been eating more snacks since the coronavirus pandemic began.

In 2019, more than 35% of extruded snack sales took place at supermarkets and hypermarkets, followed by convenience stores and online retailers. Potato-based snacks comprised more than 25% of revenues. Tapioca-based snack revenues are expected to increase at a compound annual growth rate (CAGR) of 4.1% from 2020 to 2027 due to increasing demand by younger generations for healthier snacks. Tapioca is cholesterol-free, low in sodium and free of common allergens, such as gluten and wheat. Tapioca in various forms is widely consumed in Latin America, Africa, and Asia. Europe had a more than 40% market share in 2019 owing to consumer snacking during social occasions and snacking on-the-go. The Asia Pacific region’s share is expected to increase the most, at a CAGR of 5.6%, due to the large populations in China and India and a growing corporate culture in which parties, where drinks and snacks are served, are encouraged.3 The market for extruded snacks is fragmented with many small local and international manufacturers. Major companies with large customer bases include Nestlé S.A.; The Kellogg Co.; Calbee, Inc.; PepsiCo, Inc.; and Campbell Soup Co.

1 Undernutrition includes wasting (low weight-for-height), stunting (low height-for-age) and underweight (low weight-for-age). 2 Nutrix was developed as a result of a collaboration between Vissot, Danish Care Foods, partners at UNICEF, the French National Research Institute for Sustainable Development, the University of Copenhagen, and the Department of Fisheries Post-Harvest Technologies and Quality Control, Fisheries Administration, Cambodia in addition to a grant from the Bill & Melinda Gates Foundation. 3 Any projections involving increased sales at large venues or gatherings may be less than accurate due to the disruption to the economy and daily life as governments closed businesses and imposed stay-at-home orders to slow the spread of COVID-19 in 2019 and 2020.

Geographic reference: World Year: 2019 and 2027 Market size: $51.59 billion and $74.52 billion Sources: “Extruded Snacks Market Size, Share & Trends Analysis Report by Product (Potato, Corn, Rice, Tapioca, Mixed Grains), by Distribution Channel, by Region, and Segment Forecasts, 2020 – 2027,” Grand View Research Report Summary, April 2020 available online here; “Extruded Snacks Market Size Worth $74.52 Billion by 2027 | CAGR: 4.7%: Grand View Research, Inc.,” CISION PR Newswire, April 30, 2020 available online here; “Malnutrition,” World Health Organization, April 1, 2020 available online here; “Nutrix – The Big Reach of Small Fish in Nourishing Cambodia,” CGIAR, March 31, 2020 available online here; “Food Extrusion,” Wikipedia, September 20, 2019 available online here; Carlie Porterfield, “In Coronavirus Quarantine, We’re Eating More Processed Snacks,” Forbes, April 28, 2020 available online here; Lacey Bourassa, “The Health Benefits of Tapioca,” Livestrong.com, September 16, 2019 available online here; “Snacking Motivations and Attitudes – US – January 2019,” Mintel Reports Overview, January 2019 available online here; Liz Parker, “State of the Industry 2019: Puffed and Extruded Snacks Find Growth Through Product Diversity,” Snack Food & Wholesale Bakery, July 23, 2019 available online here; Steve Dwyer, “Snacks: Diving Into Extrusion,” CSP, September 5, 2017 available online here; Sorpida Korkerd, et. al., “Expansion and Functional Properties of Extruded Snacks Enriched with Nutrition Sources from Food Processing By-products,” Journal of Food Science and Technology, January 2016 available online here; Tamar Lapin, “Americans are Handling the Coronavirus Pandemic by Binging on Snacks,” New York Post, April 13, 2020 available online here. Image source: WikimediaImages, “food-eat-diet-goldfish-crackers-2202364,” Pixabay, April 4, 2017 available online here.

“Some algae are a delicacy fit for the most honoured guests, even for the King himself.”

— Sze Teu (China, 600 BC)

Since prehistoric times, seaweed has been a staple food in China, Japan, and Korea. Commercial seaweed was first consumed in Japan in the 4th century and in China in the 6th century. Currently, China, Japan, and South Korea are the top consumers. As residents of these countries migrated to other parts of the world, demand for seaweed spread. Seaweed provides vitamins and nutrients such as calcium, sodium, potassium, iodine, iron, and zinc. Nori, the seaweed used to wrap sushi rolls, is also high in protein.

Today’s market size shows global commercial seafood revenues for 2019 and projected for 2027. Over the past 50 years, harvesting seaweed from natural sources has not been able to meet increasing demand. Nowadays, more than 90% of commercial seaweed is cultivated. In addition to human consumption, commercial seaweed is used as an animal feed additive, thickening and gelling agents for the cosmetics and food industries, fertilizer, and soil conditioner. It’s also used in beauty products such as scrubs, masks, and body wraps.

There are three types of commercial seaweed: red, brown, and green. In 2019, red seaweed comprised more than 50% of the market. Its varied uses along with its easy availability will drive its growth in the market. This type of seaweed is expected to have the highest compound annual growth rate through 2027. Nori is an example of red seaweed. Brown seaweed had a market share of more than 45% in 2019. This type of seafood is used as food and as raw materials for the extraction of hydrocolloid and alginate. Hydrocolloids and alginate gel are used for wound care. Alginate is also used as a cell carrier in tissue engineering. Kelp is a form of brown seaweed. Green seaweed is also used for food. Umibudo, also known as sea grapes, is a form of green seaweed that’s a staple food in Okinawan cuisine.

In 2019, the Asia-Pacific region accounted for more than 60% of consumption. This region is expected to experience the fastest growth rate through 2027. Increased production and demand for commercial seafood for use in food, nutraceuticals, personal care products, pharmaceuticals, adhesives, and gels from China, Indonesia, South Korea, and Japan will contribute to this growth. The market in Europe is expected to expand significantly due to increased cultivation in Ireland, France, and the United Kingdom. Growth in this region is also expected to come from high demand in the healthcare and food industries.

About 75% of commercial seaweed was used for human consumption in 2019. Animal feed claimed the second-largest share of the market. Processed commercial seaweed is used to improve the health of livestock. Agricultural uses had the third-largest market share. Producers, vendors, end-users, government organizations, and others encompass the market. Some leading global companies in this industry include Cargill Inc., Roullier Group, E.I. DuPont Nemours and Co., Biostadt India Ltd., and Compo GmbH Co.

Geographic reference: World Year: 2019 and 2027 Market size: $5.9 billion and $11.9 billion, respectively Sources: “Commercial Seaweeds Market Size, Share & Trends Analysis Report by Product (Brown Seaweeds, Red Seaweeds, Green Seaweeds), by Form (Liquid, Powdered, Flakes), by Application, by Region, and Segment Forecasts, 2020 – 2027,” Grand View Research Report Summary, April 2020 available online here; “Commercial Seaweeds Market Size Worth $11.9 Billion by 2027: Grand View Research, Inc.,” CISION PR Newswire, April 21, 2020 available online here; “Hydrocolloid,” ScienceDirect available online here; “Alginate,” ScienceDirect available online here; “Seaweed as Human Food,” The Seaweed Site: Information on Marine Algae available online here; Ole Mouritsen, “The Science of Seaweeds,” American Scientist, November-December 2013 available online here; Rachel Tan, “6 Most Common Varieties of Edible Seaweed,” Michelin Guide, June 12, 2019 available online here. Image source: ivabalk, “sushi-food-roll-domestic-production-2314534,” Pixabay, May 15, 2017 available online here.

Candy, potato chips, ice cream, popcorn, fruits, or vegetables. What comfort foods have you been reaching for in these unprecedented times? If you’re like 28% of the population, your go-to comfort food is candy, with an overwhelming majority of those choosing chocolate.

Today’s market size shows candy revenues for the 52 weeks ended March 24, 2019, in the United States. Revenues for chocolate candy, totaling $14.1 billion, exceeded 55% of total candy revenue over this time period. However, this was 1.3% lower than the previous 52 week period. Non-chocolate candy, gum, and breath freshener revenues totaled $7.4 billion, $3.1 billion, and $776 million, respectively. Sales of gum grew by 2%. Non-chocolate candy sales increased by 0.8%. But sales of breath fresheners decreased by 3.8% from the year prior.

As in other sectors of the food and beverage industry, consumers are seeking better-for-you options in the candy aisle too. For consumers, “organic” labeling implies the food is pesticide-free, preservative-free and hormone-free. To replace “natural” labeling, which many see as a gimmick, manufacturers are using “free-from” labeling, such as “GMO-free” and “gluten-free”, to communicate to the consumer that their products do not have ingredients that may be perceived as unhealthy. With low-carb diets trending, sugar-free chocolate candy saw a 19.2% increase in sales from the prior year, led in part by a 152% jump in sales of Lily’s Sweets, the number two selling sugar-free chocolate candy behind Russell Stover, which saw a 13% increase in sales.1 Consumers still consider dark chocolate healthier, but they also seek indulgence. As a result, manufacturers are combining different types of chocolate, using higher-quality, ethically-sourced ingredients, offering unique flavors, and adding nuts and fruits to their dark chocolate products.

In North America in 2019, Mars Wrigley Confectionery U.S. topped sales with $18 billion, followed by Mondelez International ($11.9 billion), The Hershey Co. ($7.95 billion), Ferrero ($2.9 billion), General Mills ($2.1 billion), Kellogg Co. ($1.89 billion), Lindt & Sprungli (North America) Inc. ($1.7 billion), Barcel S.A. ($1 billion), Clif Bar & Co. ($900 million) and KIND Healthy Snacks ($719 million). Mars Wrigley Confectionary also led in sales worldwide.2

1 Russell Stover sugar-free chocolate sales totaled $95.4 million. Lily’s Sweets sugar-free chocolate sales totaled $13.7 million. 2Candy Industry Magazine reports both North American and global sales for Mars Wrigley Confectionery as $18 billion.

Geographic reference: United States Year: 2018-2019 Market size: $25.38 billion Sources: “The State of the Global Candy Industry in 2019,” Candy Industry Magazine, June 10, 2019 available online here; Laurnie Wilson, “Infographic: Americans Say Chocolate, Chips Are Top Quarantine Comfort Snacks,” Civic Science, April 1, 2020 available online here; “Sweet 60 2019: The Top Candy Companies in North America,” Candy Industry Magazine available online here; “2019 Global Top 100 Candy Companies: Part 1,” Candy Industry Magazine available online here. Original source: IRI Image source: Patrick Fore, “Jelly Beans,” Unsplash, February 26, 2018 available online here.

Over the past several years, tortillas and tortilla chips have become staples in the retail and foodservice sectors and perhaps in your own pantry too. The growing Hispanic and Latino population in the United States, the influence of Latin American cuisine throughout the country, and the foods’ versatility have contributed to their popularity. In addition, consumers perceive tortillas as being healthier than bread. Some consumers looking for products with few ingredients and no preservatives are switching their buying habits from loaves of bread to packages of tortillas.

To capitalize on this better-for-you trend, manufacturers are making tortillas with whole wheat flour, ancient grains, plant proteins, flax seeds, and herb-based dough. Manufacturers are also creating tortillas for specific diets, such as low-carb, high-fiber, and low-calorie. Some Paleo-friendly grain-free tortillas and tortilla chips are made with cassava flour and vegetables. Others are made with nut flours. Organic, gluten-free, and non-GMO tortillas and tortilla chips are also trending among health-conscious consumers. In addition to healthy ingredients, consumers desire a variety of flavors: from traditional Latin-inspired chipotle adobo and tomatillo salsa to Mediterranean tzatziki to comfort food favorites like bacon Cheddar.

Today’s market sizes show retail sales of tortillas and tortilla chips in 2016 and 2019. Overall, revenues are expected to decline in 2020 as demand drops dramatically from restaurants that have closed or that are operating at reduced capacity during the COVID-19 pandemic. According to the Tortilla Industry Association, most of the $17.8 billion tortilla and tortilla chip sales in 2019 occurred at retail establishments (48%); followed by foodservice locations (24%) and schools, institutions, and military bases (21%). Leading tortilla manufacturers include Mission Foods, Inc.; Gruma Corp.; General Mills, Inc.; Olé Mexican Foods, Inc.; El Milagro; B&G Foods, Inc.; La Tortilla Factory; Megamex Foods; and Kraft Heinz Co. Leading tortilla chip makers include Frito-Lay, Inc.; Barcel USA; OTB Acquisitions LLC (On the Border brand); Mission Foods, Inc.; Gruma Corp.; Late July Snacks LLC; Juanita’s Fine Foods, Inc.; Xochitl, Inc.; Garden of Eatin’, Inc.; and Food Should Taste Good, Inc. For the 52 weeks ended June 16, 2019, Frito-Lay brands commanded more than 68% of the tortilla chip and tostada market.1

1 Leading manufacturers of tortillas and tortilla chips are based on dollar sales according to IRI. Tortillas: Sales at supermarkets, drug stores, mass merchandisers, convenience stores, military commissaries, and select club and dollar chains for the 52 weeks ended March 24, 2019. Melissa Kvidahl Reilly, “State of the Industry 2019: Tortillas Offer Health Attributes and Big Flavor,” Snack Food & Wholesale Bakery, June 24, 2019 available online here. Tortilla chips: Sales by brand at supermarkets, drug stores, mass merchandisers, convenience stores, military commissaries, and select club and dollar chains for the 52 weeks ended June 16, 2019. “Claim to Fame,” Snac World Special Edition: Official State of the Industry 2019, Annual 2019 available online here.

Geographic reference: United States Year: 2016 and 2019 Market size (Tortillas): $2.3 billion and $2.6 billion, respectively Market size (Tortilla chips): $4.9 billion and $5.5 billion, respectively Sources: “Tortilla Product Diversity Drives Increased Sales,” Snack Food & Wholesale Bakery, March 1, 2020 available online here; Melissa Kvidahl Reilly, “State of the Industry 2019: Tortillas Offer Health Attributes and Big Flavor,” Snack Food & Wholesale Bakery, June 24, 2019 available online here; “Claim to Fame,” Snac World Special Edition: Official State of the Industry 2019, Annual 2019 available online here; “Tortilla Production Industry in the US – Market Research Report,” IBISWorld Press Release, August 2019 available online here. Original source: IRI Image source: Ryan Concepcion, “Wrapped Food with Gravies,” Unsplash, July 2, 2019 available online here.

In the United States, December 4th is National Cookie Day. But most people don’t wait for a holiday to indulge in their favorite sweet treat. In a survey conducted by Ask Your Target Market, 22.75% of U.S. consumers reported buying cookies once a month and about the same percentage, 22.25%, reported buying cookies more than once a month.

The love of cookies extends beyond the United States. Cookies are a beloved treat all over the world. Amaretti in Italy, macarons in France, kleicha in Iraq, rafioli in Croatia, stroopwafel in the Netherlands, and chocolate chip in the United States. Cookies come in many shapes, sizes, flavors, and textures. To pique the interest of consumers, bakery manufacturers add unusual flavorings such as pineapple and chai spices to their products. However, in developed countries like the United States, Germany, and the United Kingdom, chocolate cookies continue to be highly favored. Nabisco Oreos are the best selling cookies in the world with more than $2 billion in annual sales. In 2018, Oreo sales totaled more than $698 million in the United States.

To capitalize on consumers’ health-consciousness, cookie manufacturers add oats, quinoa, and other whole grains to their products. Consumers’ concerns about gluten intolerance, especially in North America and Europe, will continue to create product demand for gluten-free products and growth in the market. Consumers’ continued demand for on-the-go foods is also expected to increase revenues in the coming years.

Today’s market size shows worldwide cookie revenue in 2018 and projected for 2025. North America, the Asia-Pacific region, and Europe were the largest markets for cookies in 2018. Cookie revenues in North America alone totaled more than a third of all worldwide revenue in this category in 2018, $10.42 billion. By 2025, 25% of worldwide cookie revenues are expected to come from the Asia-Pacific region due to rising incomes and changing lifestyles.

Most people buy cookies at supermarkets and convenience stores; however, online sales are expected to experience the fastest growth between 2018 and 2025. By 2025, nearly 20% of cookie sales are projected to take place online. Some top cookie manufacturers include The Kellogg Co.; Nestlé S.A., PepsiCo, Inc.; Britannia Industries Ltd.; The Campbell Soup Co.; Mondele̅z International, Inc.; Danone S.A.; and Parle Products Private Ltd.

Geographic reference: World Year: 2018 and 2025 Market size: $30.62 billion and $44.01 billion, respectively Sources: “Cookies Market Size, Share & Trends Analysis Report by Product (Bar, Molded, Rolled, Drop), by Distribution Channel (Offline, Online), by Region (North America, APAC, MEA, Europe, CSA), and Segment Forecasts, 2019 – 2025,” Grand View Research Press Release, April 2019 available online here; “Cookies Market Size Worth $44.01 Billion by 2025 | CAGR: 5.3%: Grand View Research, Inc.,” CISION PR Newswire Press Release, May 22, 2019 available online here; Anne Pilon, “Cookie Survey: People Buy More Cookies Over the Holidays,” AYTM, December 4, 2014 available online here; Stephanie Ashe, “13 Things You Didn’t Know About Oreo Cookies,” Insider, March 5, 2019 available online here; “2017 Fact Sheet,” Mondele̅z International available online here; “Top 50 Most Popular Cookies in the World,” TasteAtlas, November 19, 2019 available online here; “Top 8 Most Popular African Cookies,” TasteAtlas, November 19, 2019 available online here; “U.S. Cookie and Snack Sales,” The Manufacturing Confectioner, February 2019, p. 15 available online here.

Image source: Steven Giacomelli, “cookies-chocolate-chip-cookies-1264263,” Pixabay, March 18, 2016 available online here.

Whether diced in a dip, sliced in a salad, minced in stuffing, or fried atop a green bean casserole, onions are versatile vegetables that add flavor to dishes without adding many calories. Perhaps because of this, onions were the third most consumed vegetable in the United States in 2018.1 Only potatoes (113.7 pounds per capita) and tomatoes (86.1 pounds per capita) had higher consumption rates. Per capita consumption of onions totaled 22.3 pounds, the vast majority of which, 20.4 pounds, was in the form of fresh onions. Yellow onions were the most popular, 34% of sales, followed by red onions (14.3%), scallions (13.3%), white onions (11.3%), Vidalias (7.4%) and shallots (1.5%).2

Today’s market size shows the total value of utilized production in the United States for 2016, 2017, and 2018. In 2018, onions ranked 5th behind tomatoes, head lettuce, romaine lettuce, and sweet corn. In 2016, onions ranked 3rd. Most of the value comes from fresh onions. In 2018, fresh onion value totaled $655.1 million. Processed totaled $162.4. From 2016 to 2018, the price per hundredweight of harvested onions fell from $16.50 down to $13.50. Prices may increase during the 4th quarter of 2019 due to a smaller harvest in the Northwest and Rocky Mountain regions. Rain in the summer delayed planting, harvesting was delayed because of more rain and because the onions were still in the ground later than usual, a mid-October freeze may have affected 20-25% of the crop. The top three states for onion production are California, Washington, and Oregon.

1 Per capita food availability measures. 2 Market shares are based on sales at supermarkets, drug stores, mass merchandisers, military commissaries, and select club and dollar chains for the 52 weeks ended June 17, 2018. Source: Market Share Reporter, 30th Edition, Gale, a Cengage Company, 2020, pages 401-402. Original source: Fresh Foods – A Supplement to Winsight Grocery Business. Annual 2018, p. 41, from IRI.