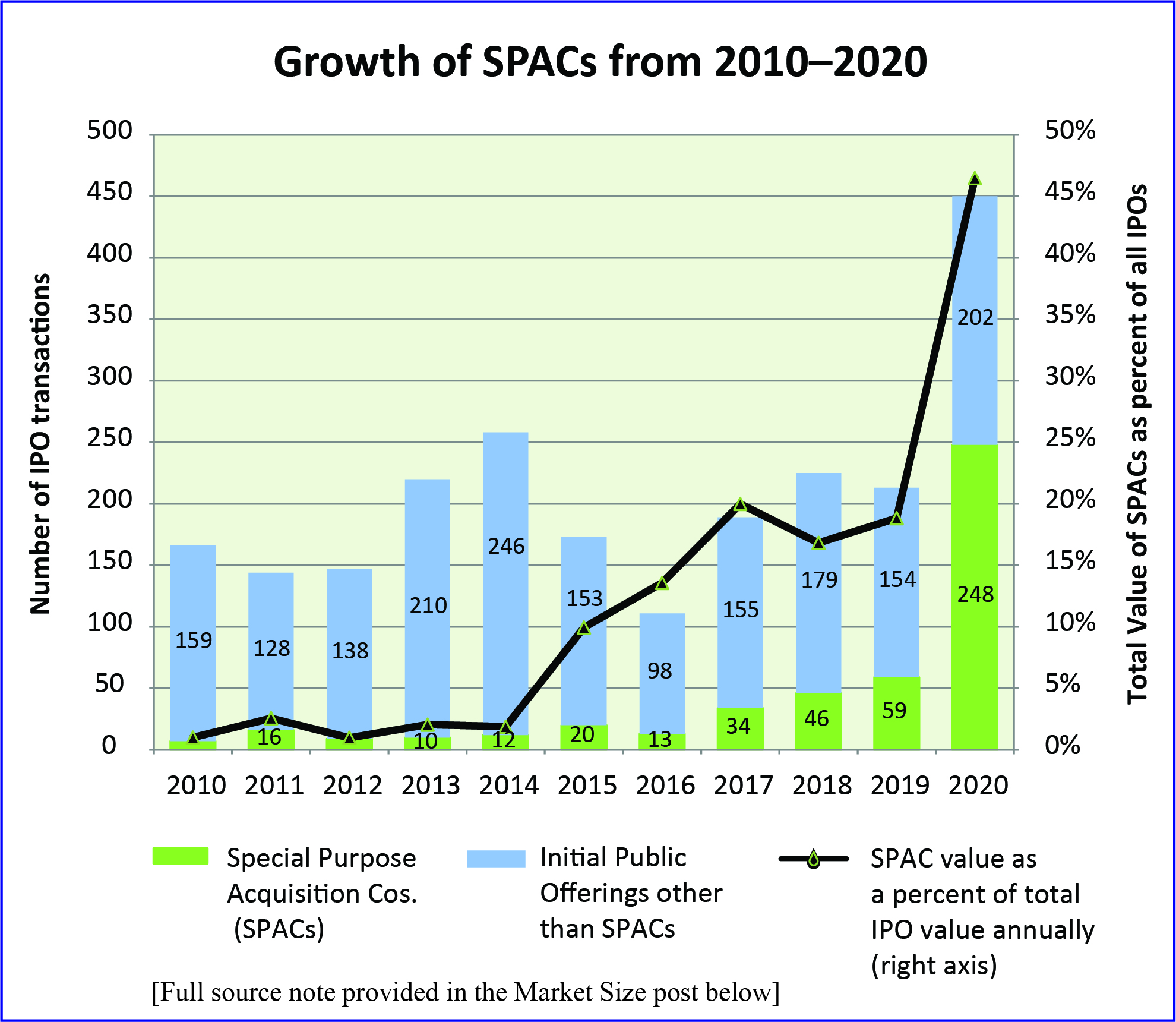

Year: All of 2020 and the first half of 2021

Market size: $2.6 billion and $2.1 billion, respectively

Not too long ago, budding entrepreneurs with a new, innovative product or service would look to a handful of wealthy investors to fund their business ventures. Because of the riskiness of investing in startups — an overwhelming majority of startups fail, with more than a fifth failing in their first year — Securities and Exchange Commission (SEC) rules restricted investments into such ventures. Accredited investors, those that were allowed to invest in startups, were limited to persons who had an income over $200,000 ($300,000 joint income), had a net worth of greater than $1 million, or be a general partner, executive officer, or director for the startup company. Startups also preferred to deal with a small number of large investors rather than spend time processing a large number of small checks.

But, this has changed for some. New technological tools, such as crowdfunding websites, make fundraising from a large number of small investors easier. And, on August 26, 2020, the SEC began allowing less wealthy investors to become accredited. Now, SEC rules allow “persons to qualify as accredited investors based on certain professional certifications, designations or credentials or other credentials issued by an accredited educational institution.” However they qualify to become accredited, angel investors provide financial backing for small startups or entrepreneurs in exchange for ownership equity or convertible debt, the term “angel” coming from the Broadway theater when wealthy patrons would give money to produce theatrical productions. Today’s market size shows the total amount angel investors invested in startups in 2020 and in the first half of 2021 in the United States.

In 2020, there were 2,725 new angel investors. This number is expected to exceed 3,000 in 2021. Most new angel investors have ties to the tech industry, but they are outsiders in the world of venture capitalists. Others come from various walks of life including doctors, dentists, art curators, professional poker players, influencers, and retirees among others. The angel investor boom is part of the larger trend of investors seeking out riskier investments in recent years. Some are taking on these riskier investments because they have extra cash to invest and want a higher rate of return than what’s offered on traditional investments. Many are investing in tech startups, seeing the high profits companies in this sector are generating. Others are motivated by causes they believe in or want to give a hand up to those generally overlooked by traditional venture capitalists, like minority and women entrepreneurs. Less than 2% of venture capital funding goes to women-founded businesses.

While accepting the risk, most of these smaller investors are not going into this venture blindly. In addition to listening to investment podcasts and reading news articles, investors have at their disposal a range of companies that offer angel investor resources to help them navigate this type of investing. For example, companies such as Angel Squad, Seed Spot, and VC Academy, among others, provide training courses for would-be angel investors. Pipeline Angels, Launchpad Venture Group, TBDAngels, and Golden Seeds are just a few of the groups that angel investors can join to lessen individual investment risk. Generally, investors who join groups don’t have to put as much money down as individual investors do, although this varies by group. Also, by being a part of a group an investor does not have to seek out and vet deals independently. Some groups decide to invest in ventures as a group, writing one check; others allow individual investors to make their own decisions. Many angel groups are centered around a certain industry or have certain requirements for the type of company in which they will invest. For example, some groups will only invest in clean energy companies, while others will only invest in BIPOC-founded companies. Some groups invest only in local companies while others work with all companies. Some of the most successful angel investors of 2020 included Fabrice Grinda, Paul Buchheit, Esther Dyson, Alexis Ohanian, and Scott Banister. Fabrice Grinda was named the top angel investor in the world by Forbes. Although it varies by angel and angel group, companies typically raise between $250,000 and $500,000 through angel investors, and those investors generally aim to recoup their investment within 3 to 5 years. Due to their risky nature, angel investments commonly represent 10% or less of an angel investor’s portfolio.

Original sources: National Venture Capital Association and PitchBook.Sources: Erin Griffith, “Even Your Allergist is Investing in Startups,” The Denver Post, reprinted from The New York Times, September 12, 2021, p. 3K; Sean Bryant, “How Many Startups Fail and Why?” Investopedia, November 9, 2020 available online here; Veronica, “Founders + Funders: Angel Investing Advice and Resources,” Medium, February 17, 2021 available online here; “SEC Modernizes the Accredited Investor Definition,” Securities and Exchange Commission Press Release, August 26, 2020 available online here; Akhilesh Ganti, “Angel Investor,” Investopedia, July 26, 2020 available online here; Adam Hayes, “Accredited Investor,” Investopedia, August 25, 2021 available online here; “Angel Investor Training,” Seed Spot available online here; “VC Angel Investor Program,” VC Academy available online here; Dylan Taylor, “The Top 5 Angel Investors,” Morgan Brooks Capital, December 18, 2020 available online here.

Image source: Markus Winkler, “White and Black Typewriter on White Table,” Unsplash, June 7, 2020 available online here.